Yes—if your business acts before March 31, you can usually cut its year-end tax bill legally. The biggest wins come from paying deductible dues on time, reconciling GST with your books, claiming depreciation on genuine business assets, writing off bad debts, structuring payroll carefully, and clearing MSME payments within the allowed timelines. The mistake most businesses make is treating tax planning as a last-week scramble. That approach misses deductions, creates reconciliation gaps, and increases the odds of disallowances or notices later. A smarter approach is to review expenses, vendor payments, capital purchases, payroll items, and compliance mismatches before the books close. Done well, year-end tax planning does more than reduce taxable income—it improves cash flow, protects deductions, and leaves you with cleaner financials for the next year. Here are eight practical moves to make now.

TL;DR: Businesses can reduce year-end tax legally by acting before March 31 on deductions, depreciation, GST reconciliation, payroll structuring, and MSME dues. The biggest gains come from planning early instead of scrambling in the last week, because missed documentation and mismatches can turn valid savings into avoidable risks. This post walks through eight practical ways to protect deductions, improve cash flow, and close the year with cleaner books.

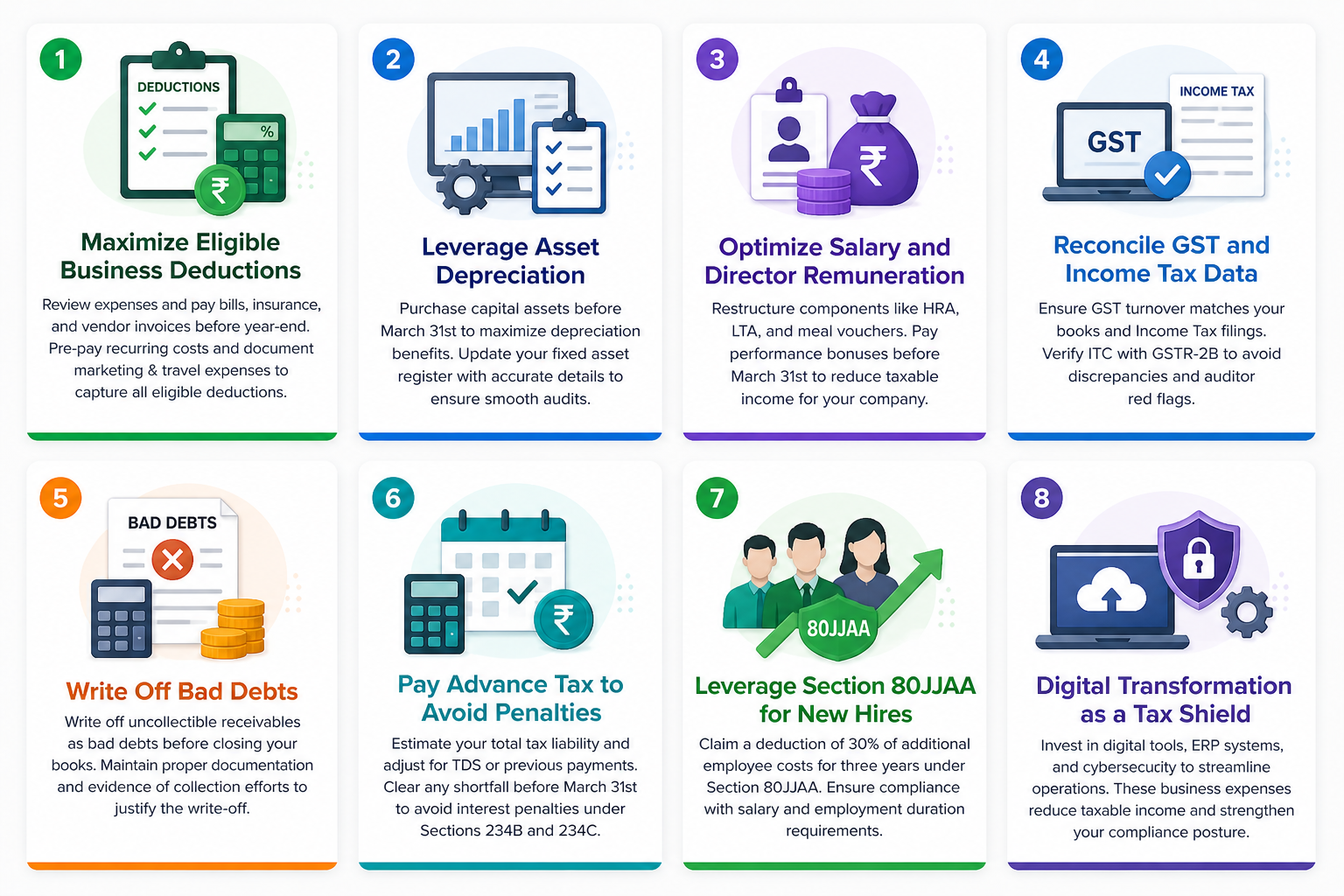

Before the year ends, review your Profit & Loss statement to ensure you have captured every legitimate business expense.

Clear Outstanding Payments: Pay off utility bills, insurance premiums, and pending vendor invoices. Under Section 43B(h), ensure you pay your MSME suppliers within the stipulated time to claim the deduction.

Pre-pay recurring costs: If cash flow allows, consider pre-paying expenses like office rent or insurance for the early months of the next fiscal year.

Marketing & Travel: Ensure all business-related travel and advertising expenses are documented with proper invoices to claim full deductions.

Purchasing capital assets—such as machinery, computers, or office furniture—before March 31st is a classic tax-saving move.

Strategic Timing: Assets purchased in the first half of the financial year qualify for full depreciation. If you buy in the second half, you can claim 50% for the current year. Plan your capital expenditures to maximize these claims.

Fixed Asset Register: Ensure your asset records are updated with correct purchase dates and classifications to avoid disputes during audits.

Structure your team’s compensation to be tax-efficient for both the company and the individual.

Component Restructuring: Review components like House Rent Allowance (HRA), Leave Travel Allowance (LTA), and meal vouchers.

Performance Bonuses: Declaring and paying performance bonuses before March 31st acts as a deductible business expense, reducing your company’s taxable income.

A mismatch between your turnover reported in GST filings and your books of account is a major red flag for auditors. The compliance backdrop is only getting tighter: according to the Press Information Bureau’s “Eight Years of GST”, gross GST collections hit ₹22.08 lakh crore in 2024–25, up 9.4% year on year, and active GST taxpayers rose to over 1.51 crore. In that environment, weak reconciliations are more likely to be noticed than explained away. If this process is still manual, structured GST filing support can help tighten return accuracy and reduce reconciliation risk.

Input Tax Credit (ITC): Verify that all claimed ITC matches your GSTR-2B data.

Turnover Sync: Ensure the revenue figures reported in your GST returns align with your Income Tax filings. Discrepancies here often lead to unnecessary scrutiny.

Practitioner note: In year-end reviews, one of the most common issues we see is revenue matching perfectly in the P&L but not across GST filings, usually because credit notes, late vendor uploads, or manual invoice edits were never tied back to the closing checklist. Teams that run a monthly GST-to-books reconciliation before March typically avoid the last-week scramble and reduce the risk of notices later.

If you have outstanding receivables that have become uncollectible despite reasonable collection efforts, you should write them off as "Bad Debts" before closing your books.

Documentation is Key: Ensure you have documented proof of the debt and evidence of your collection attempts to justify the write-off to tax authorities.

Avoid interest penalties under Sections 234B and 234C by estimating your liability against the official advance-tax schedule. Under Section 211 of the Income Tax Department, most taxpayers are expected to pay at least 15% by June 15, 45% by September 15, 75% by December 15, and 100% by March 15; taxpayers under Sections 44AD or 44ADA generally pay the whole amount by March 15.

Pre-Calculation: Estimate your total annual income and adjust for the taxes already paid through TDS or previous advance tax installments.

Clear Dues: If you find a shortfall, make the payment before March 31st to remain fully compliant.

If your business is growing and you have hired new employees, Section 80JJAA can be meaningful: eligible businesses may claim a deduction equal to 30% of additional employee cost for 3 assessment years. The official provision also excludes employees earning more than ₹25,000 per month from the definition of an additional employee, so review eligibility before assuming the benefit applies. (Source: Income Tax Department, Section 80JJAA).

Modern tax authorities use a "Trust but Verify" model. Digitizing your supply chain, implementing ERP systems, or even cybersecurity training for staff can often be categorized under business expenditures that reduce your net profit. Think of digitization not just as a cost, but as a strategic move to lower your risk profile and improve your tax efficiency.

Beyond standard deductions, Indian tax law offers specialized provisions designed to reward compliant, scaling, and innovative businesses.

Timely payment to Micro and Small Enterprises (MSEs) is a critical tax-saving strategy. Under Section 43B(h), if you fail to pay your MSME suppliers within 15–45 days, the expenditure is disallowed for the current year. You lose the deduction and must pay tax on that amount. Prioritizing these payments before March 31st safeguards your deductions and maintains liquidity. (Source: Ministry of MSME delayed-payment FAQ).

From implementation work: When we help businesses tighten their year-end close, one practical fix is to create a separate MSME dues tracker linked to invoice date, agreed credit period, and payment status. That simple control usually surfaces delayed vendor payments early enough for the finance team to act before March 31st, instead of discovering disallowances after the books are closed.

Startups often face initial losses. Income Tax laws allow you to carry forward these business losses for up to eight assessment years to offset future taxable profits. This is only permissible if your Income Tax Return (ITR) is filed before the statutory due date. If you miss the deadline, you permanently lose this future tax shield.

If you are a DPIIT-recognized startup, you may qualify for the Startup India tax holiday. Eligible startups can claim a 100% tax deduction on profits for 3 consecutive financial years out of their first 10 years since incorporation. This is not a fringe provision: according to the Press Information Bureau’s “Nine Years of Startup India”, India had 1,59,157 DPIIT-recognized startups as of January 15, 2025, and recognized startups had created over 16.6 lakh direct jobs by October 31, 2024. That makes early recognition and exemption planning materially relevant for growth-stage founders, not just a theoretical tax benefit.

When you sell capital assets (like machinery) at a profit, you incur Capital Gains Tax. You can defer or reduce this liability by reinvesting the proceeds into eligible assets or specified bonds (like NHAI bonds under Section 54EC). These strategies ensure your capital remains invested in growth rather than being eroded by taxes.

Q: Why is March 31st the most critical date for SME tax planning? A: March 31st marks the end of the fiscal year. Any expense, asset purchase, or write-off booked after this date will apply to the next financial year, meaning you cannot use it to reduce your current year's tax liability.

Q: Can I defer income to save tax? A: You can align your revenue recognition with your operational cycle, but this must be done in accordance with accounting standards. It is not about hiding income, but about reporting it correctly within the permissible frameworks.

Q: Is it smart to buy assets just to save tax? A: Only if that asset is necessary for your business growth. Never buy machinery or equipment solely for a tax deduction if it does not serve a productive, long-term purpose for your operations.

Q: How does a Virtual CFO help with tax planning? A: A vCFO doesn't just "file" taxes; they perform tax planning. They analyze your P&L throughout the year, suggest strategies like bonus payouts or asset purchases months in advance, and ensure your books are always audit-ready.

Year-end tax planning is not an accounting chore—it is a strategic business move. By being proactive rather than reactive, you retain more capital, strengthen your compliance standing, and set your business up for a stronger start to the new fiscal year. A disciplined year-end financial checklist makes that process easier to repeat every year.

Ready to close the financial year with confidence? [Click here to schedule a Tax Strategy Audit with an EaseUp expert.]

Your trusted partner for all your Financial needs.

Finance Management

Strategic Services